Original post “The EVERYTHING Short – Mortgage Edition” by zipitrealgood. This digital copy is for archive purposes and is not a financial advice.

First off, hats off to u/atobitt for creating “The Everything Short” DD. It is a good read if you haven’t checked it out. Although, like everything, don’t assume it is correct. Dive in and do your own ‘sniff test’. There was a follow up post ““The everything short continued updated again now” which delves into SPACs.

After reading these posts, I wanted to contribute an investigation into the nefarious mortgage market, specifically, looking at one of the shiny objects we were supposed to invest in…Rocket Mortgages ($RKT). My initial post gained traction and I was requested to do a separate DD by a few fellow Apes. Even though this relates to the mortgage markets, this does relate to $GME.

My Background:

Currently, I work for a FAANG company as a Data Engineer (my title is a bit more specific, but if I listed it, you would immediately know which company I work for). I am an Econ major, with a minor in Philosophy (with a focus in Logic). I spend my undergrad life learning the in’s and out’s of the ’07-’08 Housing Market crash as part of my Economics degree.

My Positions:

Read my other DD on Posting Positions. However, from my previous comments, you can ascertain that I have a significant holding in $GME (without being able to specifically understand my avg. cost, total number of shares, or even calculate a rough estimate of a ceiling or floor).

On to the DD

Summary:

- Background – The Everything Short DD

- Part I – Pre-Pandemic

- Part II – Pandemic

- Part III – Bringing it all together

TL/DR: The fucks got greedy again, there’s a massive housing bubble on top of all of this mess, and we are going to see ’08 squared.

Background:

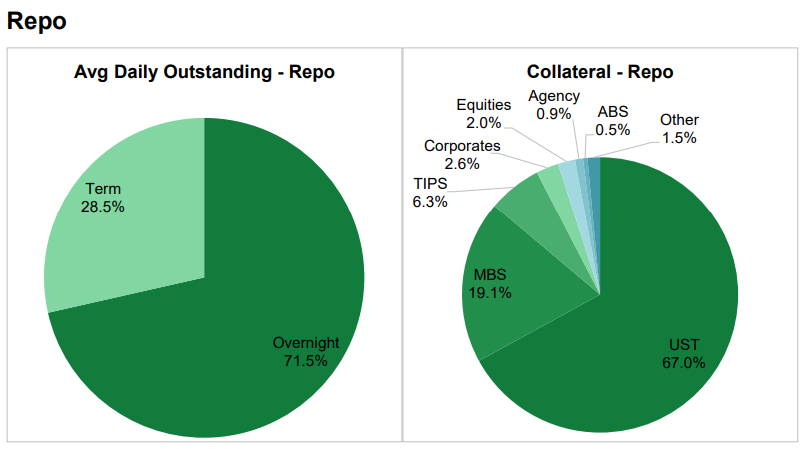

Let’s start with a pie chart that was posted in “The Everything Short” DD, which gives a good representation of how important MBS (Mortgage Backed Securities) are to the Repo market (and overall liquidity).

As you’ll see, MBS represents 19.1% of the entire Repo market, so it’s important for us to understand at a Macro-level, the health of our Mortgage lenders. As you may well know, their behavior caused the most recent market crash.

What you need to understand are that Treasury Yields are up. When Treasury Yields go up, that means higher interest rates for mortgages. When there are higher interest rates on mortgages, that means less homes sold. Less homes sold, means that mortgage lenders have less liquidity.

PART I: Pre-Pandemic

Who are the biggest Mortgage lenders in the US? – The Data I will provide will be from 2019 to use as a proxy, as I do not have the 2020 figures available to me (if an Ape has them, I’ll gladly update this DD)

Well, that’s a tough question, because it’s important how you slice the data…

First, let’s look at by purchase originations (aka the # of new loans)

- Quicken Loans (541,000)

- United Short Financial (339,000)

- Wells Fargo (232,00)

- Chase (168,000)

Okay, let’s understand by $ amount (this will include, purchase, refinance, cash-out refinance, home improvement, other)

- Wells Fargo ($306B)

- Chase ($177B)

- Quicken Loans ($146B)

Note – I know you apes want to divide $146B/541K to see how big each loan is, but you can’t. The $ amount provided includes refinance, home improvement, etc… so don’t, just be patient.

So, you might see a theme here. There are three big names. Wells Fargo, Chase, and Quicken Loans. Two of the three are LARGE banks. One, is technically defined as a “non-bank”. If you haven’t put together the pieces, Quicken Loans is that “nonbank”. Also, Quicken Loans…isn’t Quicken Loans. It’s parent company is, you guessed it, Rocket Mortgages ($RKT).

Even though Wells Fargo is a smarmy institution (Google search ‘Wells Fargo 2018’) and JP Morgan is no saint either, I want to spend my time looking into Rocket Mortgages and paint you an ugly ass picture (Bob Ross would change his mind on what a ‘happy accident’ is).

Something you need to understand is that Quicken Loans (aka Rocket Mortgages), have eyed becoming the largest Mortgage supplier to the US, which they have achieved. They represent over 9% of the total US mortgage market. Their dramatic rise is attributed to their labeling of being a “tech” focused mortgage lender who’s digital process has tapped into the millennial market. Boasting as low as 8-minutes from consumer logging on to mortgage.

Pause – Did you fucking just say 8 minutes. Yes. I did. If you are a ‘Big Short’ fan, this is the scene where they are bragging about how fast they can write mortgages. If you know anything about the financial crisis, this highlights the consumer flaw. Which was, the person requesting a mortgage, relied upon the lender to tell them what they can and cannot afford. This is a grave mistake (queue ominous foreshadowing music).

Any who, back to the numbers. With the metrics above, I’m illuminating the point that Quicken Loans is a “volume” player (feel free to look at other years, you’ll see they are just as high) not a “Quality” player. Seeing as they have a massive delta between the second mortgage supplier, and even though you can’t utilize the $ amount provided directly, they are Billions less than Chase and Wells Fargo. To prove it, here’s some fun facts about their LMI (or low to moderate income borrowers – defined as earning less than 80% of the estimated current area median family income).

In 2019, they ranked #2 with 37,252 or roughly 7% of their mortgages. Also, 70% of Quicken Loans originations were refinances (aka 70% of 541,000 is 378,000). Remember, the downside of refinancing is that it costs the mortgage owner money. Essentially, you are taking out a new mortgage to pay off the old one. A lender wants you to refinance, so they can have extra liquidity and also prevent you from moving to a different mortgage lender.

What’s the standard to get a mortgage on Quicken Loans? 580 Credit score with only 3.5% downpayment (with an option to ask for mortgage without a credit score as long as you have a phone bill and 2 other ‘verifiable’ sources of credit history). AKA, sub-prime….

Alarm bells should be ringing in your head, because the ’07 – ’08 crisis was driven by low interest rates and relaxed lending standards (incl. low down payment requirements), which allowed more people to purchase homes (or more home they could afford). This then drives home prices up, especially as people try to flip houses and extend themselves since they think “housing only goes up” (which unfortunately is amplified by companies like Zillow, who have ‘Zestimates’ which complete a self-fulfilling prophecy that an asset worth X one year is somehow worth X * (1.5 to 2.0) in a few years without any improvement).

Oh, did I also forget their Rocket Loans gem?

“Our personal loans are not secured, guaranteed or insured and involve a high degree of financial risk.

Personal loans made through our Rocket Loans platform are not secured by any collateral, not guaranteed or insured by any third party and not backed by any governmental authority in any way. We are therefore limited in our ability to collect on these loans if a client is unwilling or unable to repay them.”

If you continue to read, they define rehypothecation as a risk to these personal loans…

“Sometimes, borrowers use the proceeds of a long-term mortgage loan or the sale of a property to repay a short-term loan. We may therefore depend on a client’s ability to obtain permanent financing or sell a property to repay our short-term loans, which could depend on market conditions and other factors. In a period of rising interest rates, it may be more difficult for our clients to obtain long-term financing, which increases the risk of non-payment of our short-term loans. Short-term loans are also subject to risks of defaults, bankruptcies, fraud, losses and special hazard losses that are not covered by standard hazard insurance.”

[Chuckles] I’m in danger.

TL/DR Part I: Prior to the pandemic, Quicken Loans was riding the bull market and was dolling out “sub prime” mortgages roughly having 7% of mortgages going out to LMI (or low income) lenders. Also in their quest to become the largest mortgage lender in the US, they primarily deal in refinancing, which is a mortgage to pay off your original mortgage. They also write personal loans, which are backed up with an IOU, which they use as “collateral”. If interest rates rise, then the whole house of cards falls.

PART II – The Pandemic

Housing demand spikes because people want more space and guess who picked up the tab, seeing as they are a “Volume” player.

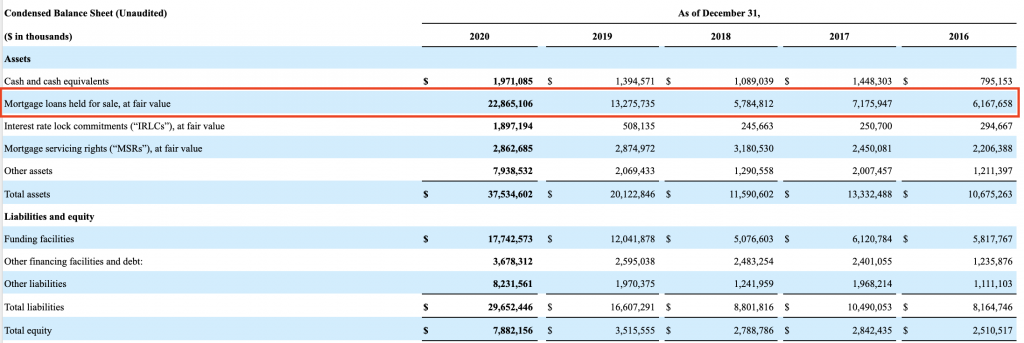

Here’s their 10-K filing in March’s Condensed Balance Sheet…

From 2019 to 2020, $RKT’s Balance Sheet goes from $13.2B to $22.8B in Mortgage loans at “fair value”. However, what should jump out to you is that cash, only increases by $580M. To put it simply, I showed this balance sheet to a CPA friend of mine (works for the big 4) without disclosing the company the balance sheet belonged to, and his quote directly was, “this is a crazy leveraged company”. Another point he brought up, “held for sale also implies they are not readily available for sale and their maturity date could be long down the road”. Therefore, their assets can’t be converted to cash quickly. Remember “The Everything Short DD”, how do you convert an asset quickly to cash? The Repo Market. Do the math there.

Also, remember, the majority of their “Volume” in 2019 were refinances (think strip club in the ‘Big Short’). Yes there was an increased demand in 2020, but you have to imagine that over 50% of their increase were also due to refinancing opportunities.

Now, here’s one of the most important quotes in their 10-K

“As of December 31, 2020, we had approximately 80,000 clients on forbearance plans, which represents approximately 3.9% of our total client serviced loans portfolio. Our delinquent loans (defined as 60-plus days past-due) were 3.91% of our total portfolio. Excluding clients in forbearance plans, our delinquent loans (defined as 60-plus days past-due) were 0.84% as of December 31, 2020. We monitor the MSR portfolio on a regular basis seeking to optimize our portfolio by evaluating the risk and return profile of the portfolio. As part of these efforts we sold the servicing on approximately 240,000 loans with $90.8 billion in UPB during the year ended December 31, 2020. These sales were more than offset by new loans that were added to the MSR portfolio organically during the period.”

APE LANGUAGE – 4% of our clients are about to be foreclosed, but not to worry, these 4% make up anyone who is 60-days past due. Since our risk team said, WOAH, this is crazy, we sold the rights to $91B to another mortgage lender but not to worry, we offset this by just creating new loans…

THAT IS SCARY. Wrote and sold the rights to $91B…aka just pawned it off

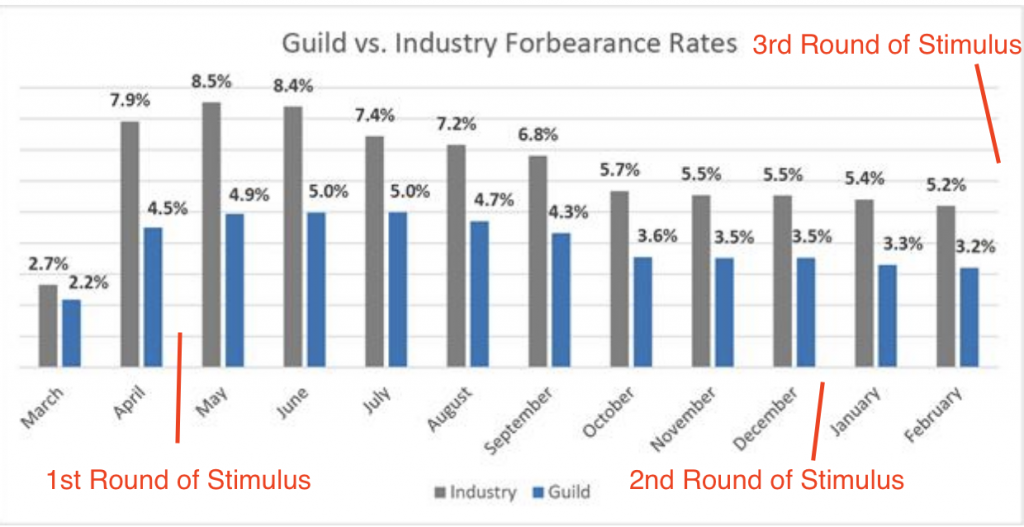

Okay, but you might say, 4% ain’t bad right? What’s the industry standard? Well, we can look to Guild Holdings ($GHLD) 10-K filing to learn more. Below, I’ve included Guild vs Industry Forbearance Rates (with stimulus injections), and unemployment graphs for your viewing pleasure.

MBA Data vs Guild Holdings ($GHLD):

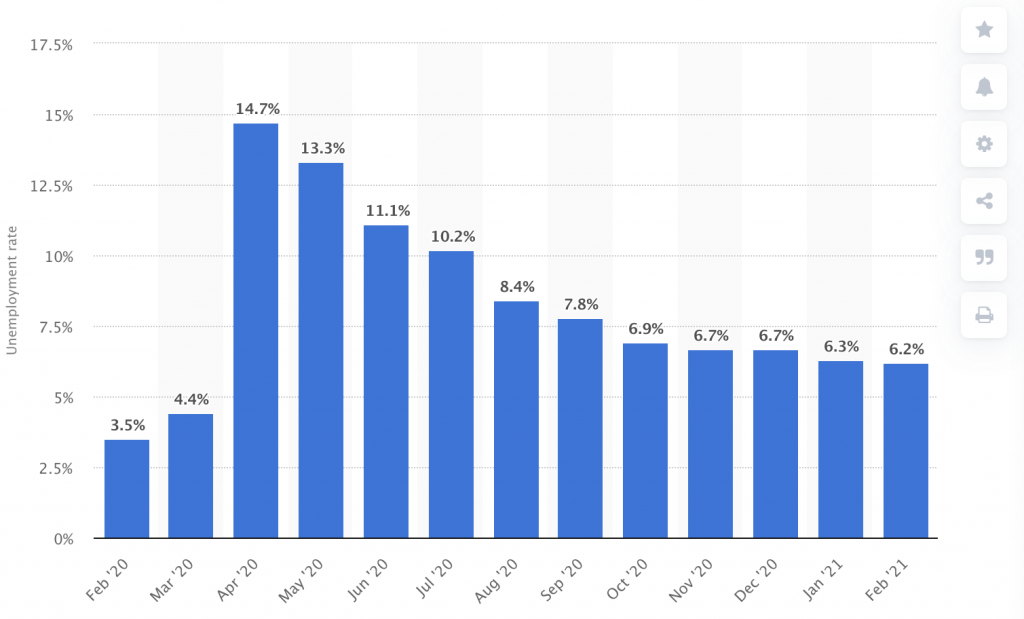

Unemployment Rate 2020:

You’ll see the industry, is not doing well. From April 2020 through February 2021, the Forbearance Rate is above 5%. Also, unemployment correlates to industry Forbearance Rates. Also, what you can see, is that a round of stimulus checks hit American wallets BEFORE Dec 31st, 2021 (I know by drawing is s$%# but common, the date was December 29th). Which skews $RKT’s claim that by Dec 31st, only an additional 1% of their loans were delinquent.

Why do I mention this?

Well, what’s important to note is that Forbearance is still 2.5% higher than pre-pandemic. This is also with the Forbearance and Foreclosure Protections for Homeowners still in effect. Which extends the foreclosure moratorium, extends mortgage payment forbearance enrollment, and provide up to six months of additional mortgage payment forbearance (if you entered forbearance on or before June 30th, 2020). Also, if you delve further into the links, you’ll see that Rent payments are behind (9%-28% by state or 1 in 6 adult renters) and 10.6M adults are in households that aren’t caught up on mortgage payments.

TL/DR Part II: Rocket Mortgages is a crazy leveraged company, who is participating in an industry that is staring down the barrel of foreclosures, only to be held off by stimulus bills and executive orders. This is not just a Rocket Mortgage issue, but an industry wide issue.

PART III – Putting it all together

Rocket Mortgages is a highly leveraged company, who’s own 10-K filing suggests that they are a ticking time bomb to destruction, and is being pushed by MSM as a “BUY” by CRYMER. Which should give you complete confidence that any “anti” Cramer play around that time (cough $GME), is the right call.

But you might say, I don’t believe this can be a whole industry thing… I still don’t believe you. Even if Rocket Mortgages goes under, we have to be fine. Right?

Well, remember CDO’s? [Sarcastic response, ‘yeah but they don’t exist anymore’]

Remember when Selina Gomez described a ‘Synthetic CDO’ and Mark Baum realized the system was imploding?

They can’t exist can they?

Well, that market can’t be big right? Everyone with a brain knows that’s a dumb investment. Can anyone be that greedy?

Well, what was the foreclosure rates in 2007 before the crash, 5.2% in 2021 ain’t bad right? Let’s use sub-prime as a benchmark since they are the worst.

In conclusion, with the largest mortgage lender leveraged to the max, reports showing that the industry is experiencing the same hardship (and if you look at GHLD’s 10-K) and are over-leveraged with the recent spikes in housing demand due to COVID. The 19.1% represented in “The Everything Short DD” Repo market of MBS is built on a house of cards. CDO’s are back, synthetic CDO’s are back, and they are getting greedier and greedier by the minute.

The rise in Treasury Yields will cause the mortgage interest rates to rise, the mortgage interest rates rising will slow down sales / refinancing opportunities, drying up liquidity for mortgage lenders (like Rocket who DEPEND on sales & refinancing to stay afloat), and the underlying assets will eventually be devalued not only by a saturation of the market naturally, but because of the influx of foreclosures that are bound to hit the market.

I completely agree with “The Everything Short DD” that $GME remains as one of the sole hedges against the implosion of the market.

TL/DR: To top it all off, we have a housing bubble, with mortgage lenders who are over extended due to the increased demand of the COVID crisis. Rocket Mortgage = New Century, they are tip of the over-leveraged iceberg. With the rise of the Treasury Yields, we’ll also see a collapse of MBS’s, which is going to cripple the liquidity of the Repo market. I agree with “The Everything Short DD” that $GME is one of the only hedges against the implosion of the market.

Thank you for reading, please let me know if I have errors, mistakes, or edits I need to make. I’ve been staring at databases for far too long today and I’m a few margarita’s in.

Obligatory: GME TO THE MOON ???? ???? ???? ???? ???? ???? ???? ???? ???? ???? ???? ???? HODL

Other Points I wanted to incorporate:

- RKT Owner, Wife, and Brother each sold 20M shares recently to get a 1.5B parachute, they found their bag holders during the pump and dump (welcome to Bear Sterns 2.0 with Crymer), and are slowly liquidating their ~1.9B now ~1.8B Class D shares

- GHLD is also leveraged crazily

- If you look at the “other assets” of the condensed RKT balance sheet, they are primarily (5.7B) in “loans subject to repurchase right from Ginnie Mae (These are also written as Liabilities, seeing as they don’t want to be a Lehman Brothers… i know its not the same thing, but you catch my drift. It can be either an asset or a liability, they don’t know yet… but spoiler… it’s a liability)

- Blackrock does have a stake in RKT, but I believe they have decreased their stake in their last filing (Please other apes, help me with this, I’ve been getting mixed data from so many sources. I didn’t include it because I didn’t have enough valid data. But I did want to highlight this as a plus for $GME, that one of the longs on $GME is winding down their position in $RKT)